The article discusses the purpose and process of closing entries in accounting, emphasizing their role in resetting temporary accounts and transferring balances to retained earnings. It also distinguishes between temporary and permanent accounts to ensure accurate financial reporting for future periods.

Journal entries prepared at the end of the accounting period to zero out the revenue, expense, and dividend accounts so accounting can begin for the next period.

To complete the accounting cycle, closing entries must be journalized and posted. In adjustable Trial Balance, we processed the transactions for Bold City Consulting and prepared the financial statements at the end of March.

If we continue recording information in the revenue, expense, and dividend accounts, we will lose track of what activity happened before April compared with what happens in April and beyond, making it impossible to prepare accurate financial statements for the next accounting period.

So the transactions from the two different periods are not confused, the revenue, expense, and dividend accounts must be reset to zero before we start recording transactions for April.

Because we must keep the accounting equation in balance, we cannot just erase the balances in the revenue, expense, and dividend accounts because it would cause the equation to become unbalanced. To keep the accounting equation in balance and still be able to zero out these accounts, accountants use closing entries; these entries accomplish two things:

- The revenue, expense, and dividend account balances from the current accounting period are set back to zero so accounting for the next period can begin.

- The revenue, expense, and dividend account balances from the current accounting period are transferred into Retained Earnings so the accounting equation stays in balance. Transferring the revenue and expense account balances into Retained Earnings actually transfers the Net Income, or Net Loss, for the current period into Retained Earnings. Transferring the dividend account balance into Retained Earnings decreases Retained Earnings by the amount of dividends for the period.

Temporary Accounts

The revenue, expense, and dividend accounts are known as temporary accounts. They are called temporary because they are used temporarily to record activity for a specific period (the accounting period), and then they are closed into Retained Earnings.

Before closing the temporary accounts, the accounting equation for a corporation would be as follows:

After closing the temporary accounts, the accounting equation would be as follows:

Permanent Accounts

The accounts that remain in the accounting equation after closing are called permanent accounts. Assets, liabilities, common stock, and retained earnings are not closed at the end of the period because they are not used to measure activity for only one specific period.

Three Closing Entries: Revenues, Expenses, and Dividends

To journalize closing entries, complete the following steps:

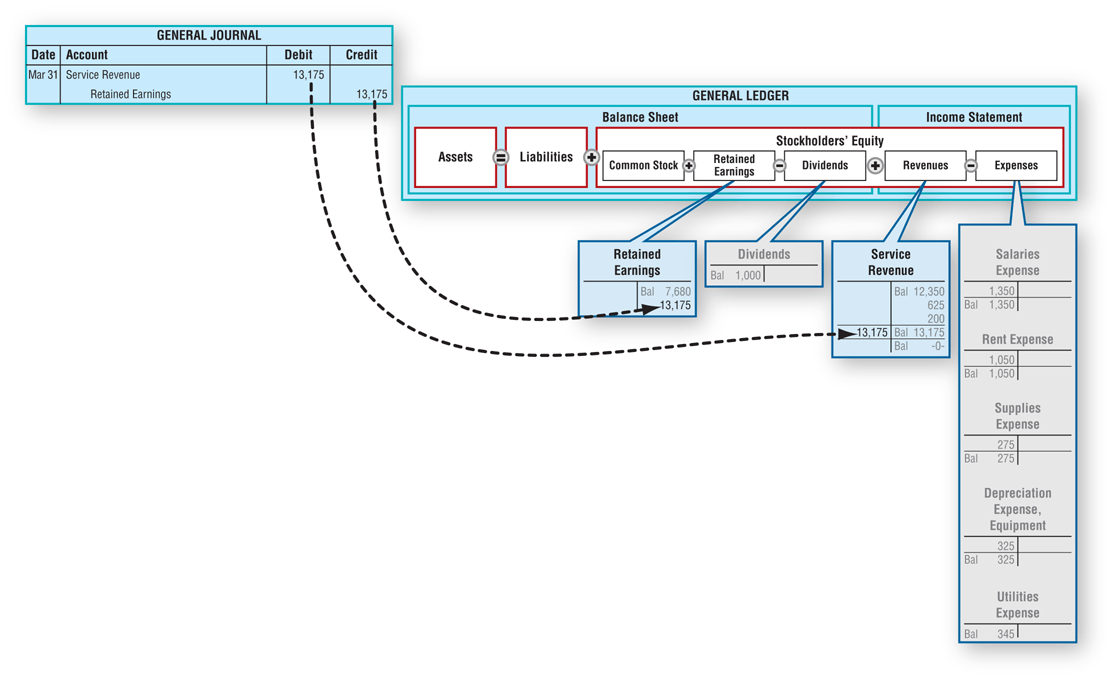

- Step 1 Close the revenue accounts and move their balances into the Retained Earnings account. To close revenues, debit each revenue account for the amount of its credit balance. Transfer the revenue balances to Retained Earnings by crediting the Retained Earnings account for the total amount of the revenues. This closing entry transfers total revenues to the credit side of Retained Earnings.

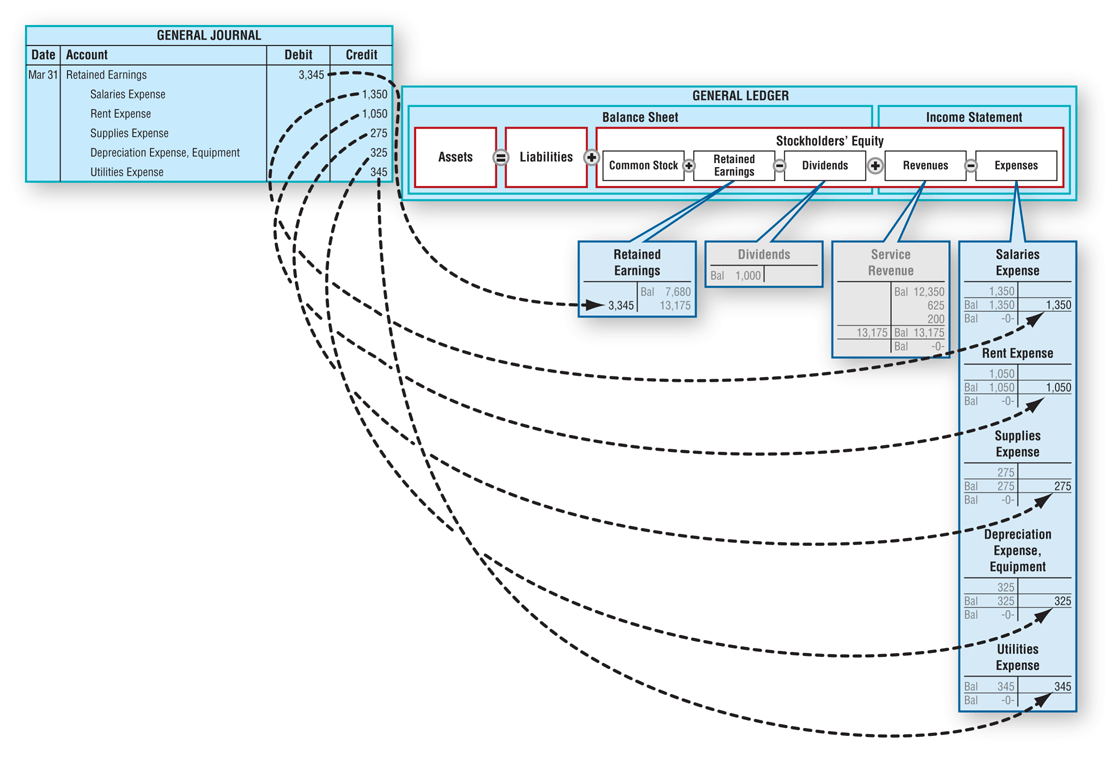

- Step 2 Close the expense accounts and move their balances into the Retained Earnings account. To close expenses, credit each expense account for the amount of its debit balance. Transfer the expense balances to Retained Earnings by debiting the Retained Earnings account for the total amount of the expenses. This closing entry transfers total expenses to the debit side of Retained Earnings.

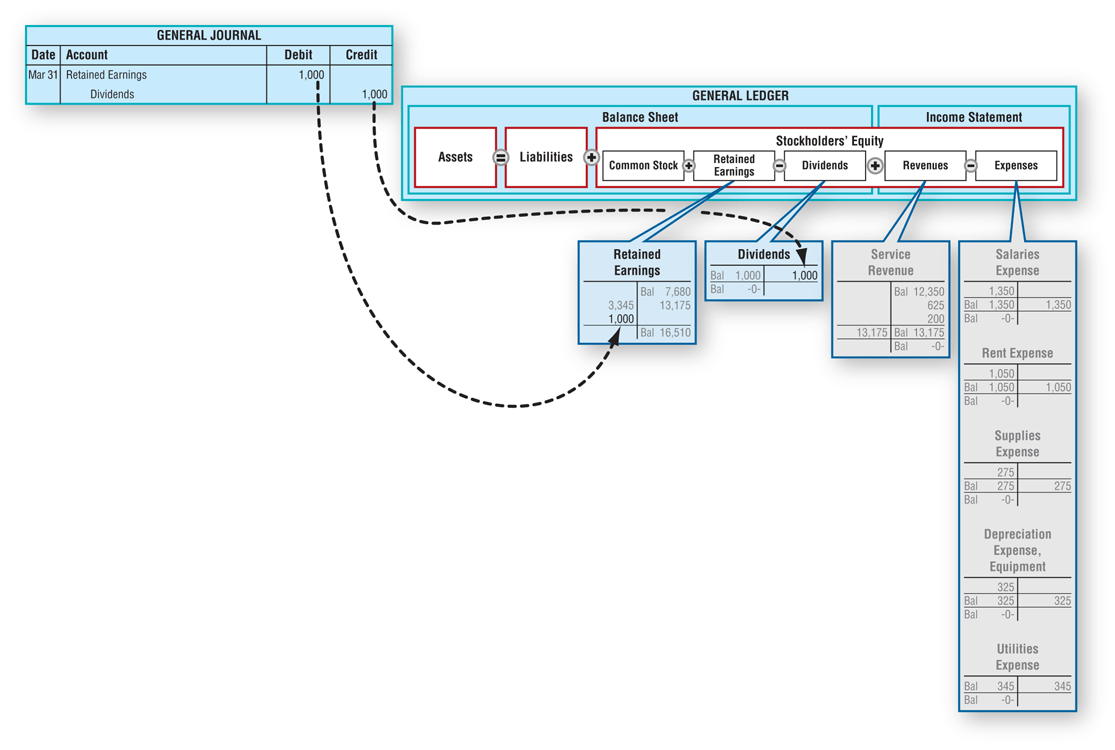

- Step 3 Close the Dividends account and move its balance into the Retained Earnings account. To close the Dividends account, credit it for the amount of its debit balance and debit the Retained Earnings account. This entry transfers the dividends to the debit side of Retained Earnings.

Now, let’s apply this process to Bold City Consulting, Inc., at the end of March:

Step 1

Step 2

Step 3

At this point, the Retained Earnings account balance reflects all the net income earned, net loss incurred, and dividends paid during the life of Bold City Consulting, Inc., to date.

Closing Entries Key Takeaways

Closing entries are essential in accounting as they ensure the accurate separation of financial activity by resetting temporary accounts and updating retained earnings. This process not only maintains the balance of the accounting equation but also prepares the books for the next accounting period, allowing for clear, consistent, and reliable financial reporting across multiple periods.