The article discusses the purpose and key users of managerial accounting information, highlighting its role in decision-making, performance monitoring, and problem-solving. It emphasizes that the relevance of such information varies by organization and user level, from line workers to strategic decision-makers.

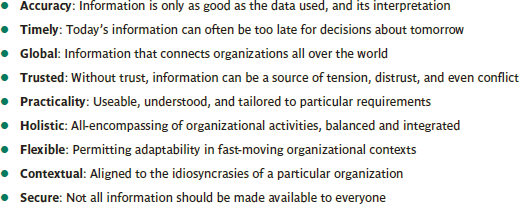

There is no general template for what constitutes ‘right’ or ‘proper’ managerial accounting information for an organization. However, certain qualities and characteristics might be generalizable to an extent (see Figure 1).

Managers attempt to make ‘right’ decisions based on the information at their disposal. But this scenario does not guarantee the ‘right’ (or ‘successful’) outcome. On the basis of information at their disposal, managers can make what they think is the ‘right’ decision but which leads to below-expectation outcomes; conversely, they can make seemingly ‘poor’ decisions which lead to better-than-expected outcomes.

Figure 1: The qualities and characteristics of useful managerial accounting information

What constitutes relevant and useful information is unique and specific to every organization, its stakeholders and its different actors; and these things can also change over time and in response to multiple outside factors. However, overlaps and common practice inevitably exist in some managerial accounting – for instance, it is not unusual to observe common managerial accounting practices among the different subsidiaries of a multinational organization.

Every organization will still have specific information needs which, in turn, shape the idiosyncratic nature of what constitutes ‘relevant’ information.

One approach to decipher what might constitute relevant managerial accounting information in a particular context might be to consider two aspects: (1) what is the purpose of such information, and (2) who are the main users of information.

Purpose of Managerial Accounting Information

While not necessarily an exhaustive list, a typical portrayal of the purpose of managerial accounting information could be a combination of the following:

- Scorekeeping: Routine recording and calculation of organizational activity over time, now increasingly undertaken ‘automatically’ by computer systems.

- External reporting: Provision of some managerial accounting information for use in external reports such as the ‘Annual Report’.

- Attention directing: Routine reporting and analysis of performance across different organizational activities, and identifying areas that might warrant some action.

- Problem-solving: Routine and ad hoc investigation of different courses of action in an organization, judging different potential outcomes and choosing the preferred option.

Key Users of Managerial Accounting Information

When considering the main users of managerial accounting information, we might think of the following:

- Line workers: This concerns either routine or ad hoc use of information to assist those below managerial level to undertake their localized and day-to-day activities, but still aligned to broader and strategic organizational goals.

- Operational managers: This concerns information normally used by middle/lower managerial to oversee that short-term organizational activities are in line with more strategic objectives.

- Strategic decision makers: This concerns information for the executives and managers at the higher level of an organization, whose primary task is to establish and monitor the goals and achievements of an organization over longer periods.

We should, however, at this point, remind ourselves that managerial accounting information comprises only a part of an organization’s entire information base.

Managerial Accounting Information Key Takeaways

Understanding the purpose and users of managerial accounting information is essential for ensuring that decisions at all organizational levels are informed, timely, and aligned with strategic goals. By tailoring information to specific users—whether line workers, operational managers, or strategic leaders—organizations can better support planning, control, and problem-solving processes. This targeted approach enhances overall effectiveness, helps allocate resources efficiently, and ultimately contributes to improved organizational performance in a dynamic business environment.