The article compares job order costing and process costing, explaining how each method is used to allocate costs based on the nature of the products or services—customized versus standardized. It highlights the key differences in application, depending on whether the output is unique or uniform.

Imagine that you go out to dinner with a friend. You are on a limited budget, so you order the cheapest thing on the menu and a glass of ice water. Meanwhile, your friend orders two drinks, an appetizer, entrée, and dessert. When it is time to pay the bill, would it make more sense to split the check equally or get a separate bill for each person at the table?

This simple scenario highlights the basic difference between job order and process costing.

Process costing is similar to splitting the check, where the total cost is spread equally over the number of units (or in the case of a meal, the number of people at the table). This simple method works well as long as the cost of each unit (or meal) is about the same.

With job order costing, a separate cost record is kept for each unique product or customer, similar to getting separate checks at a restaurant. This method makes sense when some products or customers are more costly to produce or serve than others. Job order costing is used by companies that provide customized products or services, such as a house flipping business, a custom cabinet manufacturer, or interior design firm.

Process Costing

Process costing is used by companies that make standardized or homogeneous products or services, such as:

- Coca-Cola beverages.

- Kraft macaroni and cheese.

- Charmin toilet tissue.

- Exxon petroleum products.

These and many other common products are produced using a standardized production process so that each unit of the product is identical to the next. Because each unit is the same, companies that make these products do not need to track the cost of each unit individually.

Instead, process costing breaks the production process down into its basic steps, or processes, and then averages the total cost of each process over the number of units produced. The basic process costing formula is

\[\text{Average Unit Cost=}\frac{\text{Total Cost}}{\text{Total Units Produced}}\]

Job Order Costing

Job order costing is used in companies that offer customized or unique products or services. Unlike process costing, in which each unit is identical to the next, companies use job order costing when each unit or customer differs from the next. Examples include:

- A custom home built by Toll Brothers.

- A 747 aircraft built by Boeing.

- A royal wedding gown designed by Alexander McQueen.

- An audit performed by PricewaterhouseCoopers.

Job order costing is also used by service companies that serve clients or customers with unique needs. For example, law firms, architects, and medical professionals have accounting systems to track the costs of serving individual clients. Although it might not be called job order costing, the basic approach is the same.

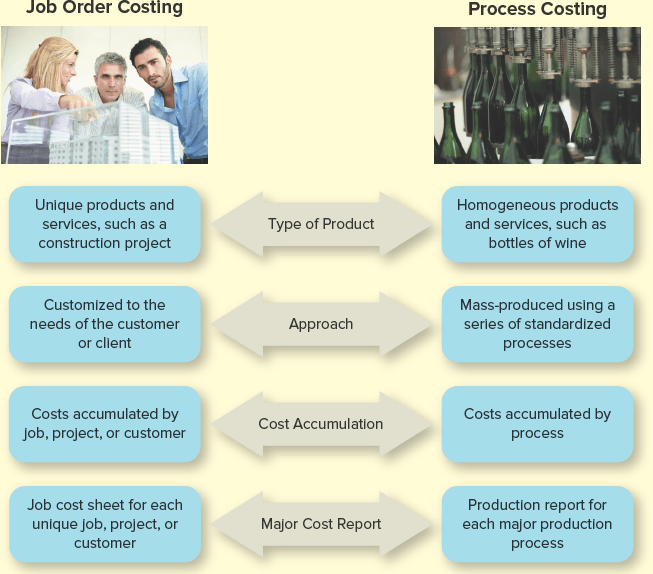

The key difference between job order and process costing is whether the company’s products or services are heterogeneous (different) or homogeneous (similar). See Figure 1 for a summary of other differences between job order and process costing.

Figure-1 Job Order Costing versus Process Costing

Job Order Costing versus Process Costing Key Takeaways

Understanding the distinction between job order costing and process costing is essential for selecting the appropriate cost accounting method based on the nature of a company’s operations. Applying the correct system ensures more accurate cost tracking, better pricing strategies, and improved decision-making, ultimately contributing to operational efficiency and financial control in both manufacturing and service industries.