The article explores Kaizen budgeting, a budgeting approach rooted in the philosophy of continuous improvement, where cost reductions and process enhancements are gradually integrated into the budgeting process. It highlights its relevance in quality-driven environments, especially in manufacturing, and notes the cultural commitment required for successful implementation.

Kaizen budgeting is budgeting based on a continuous improvement philosophy. Seeking small improvements in the operating processes which are recorded within the budget statement.

Kaizen budgeting is part of the continuous improvement philosophy. This type of budgeting works within organizations that use quality systems working towards continuous improvement.

Kaizen budgeting Example

An example of a company which implemented this type of system is Toyota. Any cost reductions, found through their drive to improve quality, would be accounted for on a continuous basis within their budgeting systems.

Rather than maintaining one set of predetermined costs at the beginning of the budgeting period, the budget embeds a reduction in operational costs as they occur. However, it is important to understand from a budgeting process, it can be very successful, especially in manufacturing organizations which are producing products on a daily basis.

The process of Kaizen budgeting requires a manager to continually identify areas of improvement within the process of manufacturing. This is achieved by seeking small changes to every process within the production line.

Although the ultimate outcome is based on cost reductions, this is more within an accounting technique; Kaizen techniques are part of a cultural mindset. Everyone working with the environment should recognize that every process can achieve small improvements on a continuous basis. Therefore, for Kaizen budgeting to be successful it needs the full support of everyone working within this environment.

Advantages and Disadvantages

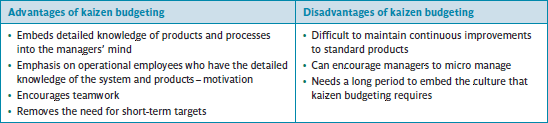

See Figure 1 for advantages and disadvantages of Kaizen Budgeting.

Figure 1: Advantages and disadvantages of kaizen budgeting

Kaizen budgeting Key Takeaways

Kaizen budgeting is important in practical applications because it aligns financial planning with continuous operational improvements, making it especially valuable in manufacturing and quality-driven environments. By embedding incremental cost reductions into the budgeting process, organizations can enhance efficiency, foster a culture of innovation, and maintain a long-term competitive advantage through sustained process enhancements.