The article discusses standard costing and variance analysis, focusing on their roles in estimating costs, decision-making, and performance evaluation. It highlights how these tools aid in planning, motivation, control, and financial reporting by comparing standard costs with actual outcomes.

Standard costs are expected costs under normal conditions, and refer to one unit of activity (for example, one unit of product or service). You can think of standard costs as the budget to produce one unit.

Being defined on a per unit basis of activity makes standard costs different from budgeted costs, which are expected costs of the entire level of activity.

To estimate budgeted costs for a given product, you draw on the standard costs of each unit to estimate total expected costs for the total number of units at stake. For example, if the standard cost of producing one unit of a particular microwave is 50 dollars, the budgeted cost of an order of 100 microwaves is 5,000 dollars.

Variance Analysis is used to compare the standard cost with the actual cost of producing an order (that is, to calculate the variances) and identify the ‘real-life’ factors causing the differences.

When variances are unfavorable (for example, actual cost is higher than the standard cost), you must identify and solve underlying problems. When variances are favorable, you should learn how to sustain that good performance, and even transfer that knowledge to other areas of the organization.

Uses of Standard Costing and Variance Analysis

Standard costing and variance analysis have been popular given their multiple applications:

Decision making.

Standard costs provide a basis for decision making, since they provide readily available estimates of future costs. For instance, to decide on future transactions, estimates of future costs are more relevant than past costs, which may not be repeatable. Although pricing must evaluate far more than just cost issues, cost estimates are important in deciding whether to accept or reject orders at a given price, to bid and negotiate prices and when prices are defined on a cost-plus basis.

Variances may also suggest strategic changes. Suppose variances indicate that prices of a new product are falling below estimates. The product manager should question if market research failed to anticipate the value perceived by customers, and should call for product redesign; alternatively, competition may have become more intense and the market strategy may have to be adjusted.

Planning, Motivation, Performance Evaluation and Control.

Standards are objectives, or benchmarks, to be achieved. Unit level standards are essential in producing budgets, in particular flexible budgets – a popular planning and control tool to produce budgets for different activity levels and product mixes. Flexible budgets enable meaningful variances to be calculated, comparing actual costs with budgeted costs for the actual level of activity and product mix.

Variance analysis can provide insights to control and assist performance evaluation. So, standards and variance analysis are important motivation tools, setting objectives and monitoring and rewarding performance.

Reporting.

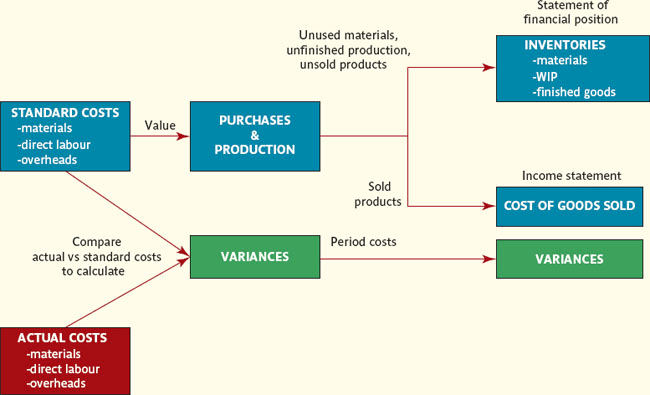

Standard costs make calculating profits and valuing inventories simple. Figure 1 describes the usual approach in valuing both purchases and production at standard costs. So, cost of goods sold and end of period inventories are also valued at standard costs, in the income statement and in the statement of financial position, respectively.

Variances between actual and standard costs are recorded separately and directly affect the income statement. Standard costs are a simple basis on which to value quantities and avoid the need to trace actual costs to individual products.

Figure 1: Standard costing valuation and variances

Standard Costing and Variance Analysis Key Takeaways

Standard costing and variance analysis are essential tools for modern business operations due to their wide-ranging applications in decision-making, strategic planning, performance evaluation, and financial reporting. By providing a structured way to estimate, monitor, and control costs, these methods help organizations enhance efficiency, identify areas for improvement, and support informed management decisions that drive long-term success.