Typical business assets are divided between non-current assets, which are expected to be retained by the business for at least a year and are of significant value, and current assets, which might change frequently during the course of the business’s activities.

Types

Most businesses own at least one of the following types of non-current assets:

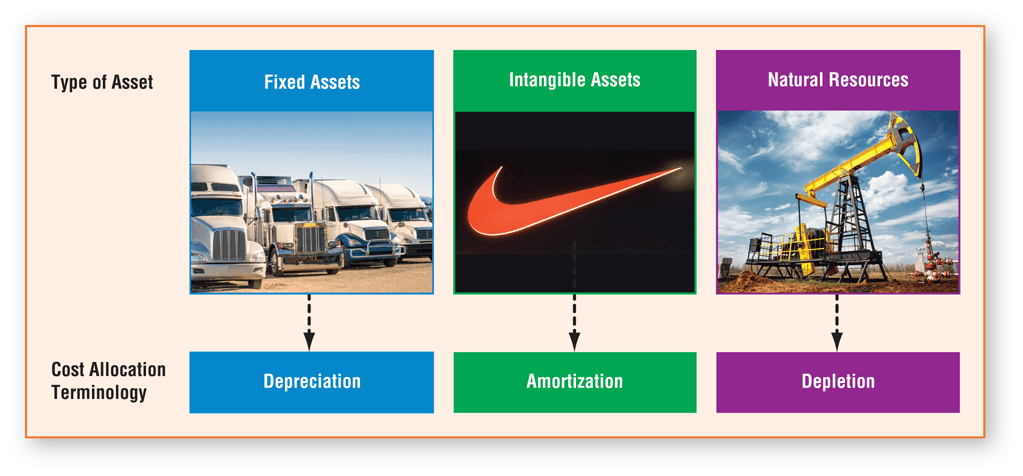

Fixed (Tangible) Assets.

Fixed assets, often called plant assets, are “physical” assets, meaning they can be seen, touched, or held. This includes assets such as land, buildings, vehicles, desks, and equipment. Fixed assets are also sometimes referred to as tangible assets.

Intangible Assets.

Patents, trademarks, and goodwill are examples of intangible assets. Unlike fixed assets, intangible assets cannot be seen, touched, or held. For example, even though a piece of paper may provide written evidence of a patent, the paper is not the patent. The patent (the intangible asset) is actually the specific rights that are conveyed to the patent owner.

Natural Resources.

Assets that come from the earth and can ultimately be used up are called natural resources. Timber, oil, minerals, and coal are all examples of natural resources.

The cost of a non-current asset must be allocated to an expense as the asset is used up. Although the process of cost allocation is similar for the different types of assets, the terminology used to describe the process is different for each. Figure 1 summarizes the different asset types and the cost allocation terminology used with each.

Figure 1: Non-Current Assets Types

Companies may also own assets that are classified as other assets. Other assets typically consist of investments made by a business.