The article explains the purpose and timing of a post-closing trial balance, which is prepared after closing entries are made at the end of an accounting period. It emphasizes that only permanent accounts are included, ensuring the ledger is ready for the next accounting cycle.

A list of the accounts and their balances at the end of the accounting period after closing entries have been journalized and posted.

The accounting cycle ends with the preparation of a post-closing trial balance. This trial balance lists the accounts and their adjusted balances after closing.

Only assets, liabilities, common stock, and retained earnings appear on the post-closing trial balance.

No temporary accounts—revenues, expenses, or dividends—are included because they have been closed. The accounts in the ledger are now up to date and ready for the next period’s transactions.

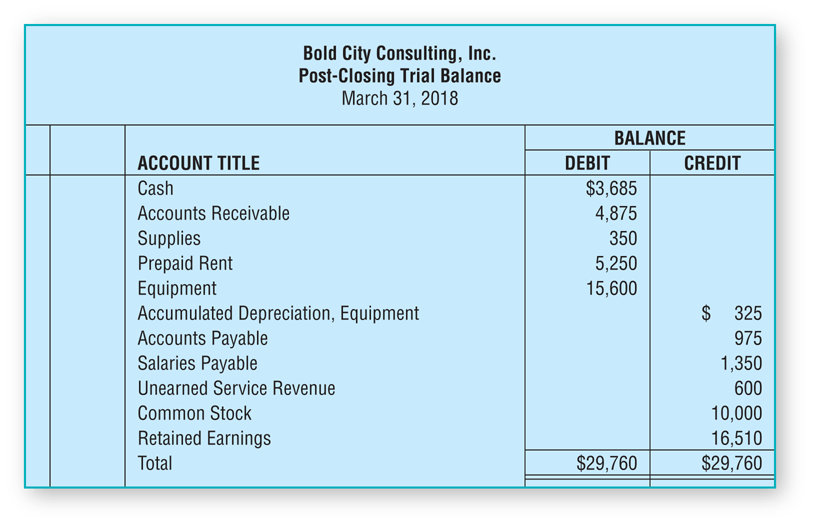

Post-Closing Trial Balance Example

The following post-closing trial balance was prepared after posting the closing entries of Bold City Consulting to its general ledger and calculating new account balances.

Figure 1: Post- Closing Trial Balance

Post-Closing Trial Balance Key Takeaways

The post-closing trial balance is essential for confirming that all temporary accounts have been properly closed and that the remaining account balances are accurate and ready for the next accounting period. This ensures the integrity of financial data, supports the smooth transition into a new cycle, and provides a reliable starting point for recording future transactions—crucial for maintaining consistent and accurate financial reporting.